Wash Trading is a form of market manipulation carried out to increase the volume of a financial instrument artificially to make it look like it is traded more than it is so investors are drawn in.

Wash Trading is a form of market manipulation carried out to increase the volume of a financial instrument artificially to make it look like it is traded more than it is so investors are drawn in.

Globally, regulators have been clear that this form of market abuse is illegal and undermines the confidence in the financial markets. Financial firms have both compliance and ethical obligations to prevent Wash Trading by their employees and their clients. They need to be able to detect this activity and should it occur, report any market manipulation to the regulator.

Topics Covered:

What is Wash Trading?

In Wash Trading, an individual tries to create artificial trading volume in a security so that it appears as though there is a “buzz” around it, which will then inflate the volume.

Price movement is not the main driver in Wash Trading - the manipulation could affect the price but it may not. The intention with Wash Trading is to increase the volume traded for an instrument, thus making it appear more liquid.

Working with another trader or using an account of their own, the individual buys and sells the security repeatedly and rapidly. The trades themselves have no economic purpose since they are very close in price and quantity to the chosen security.

The individual will then be able to draw attention to the security, thanks to the increased volume pattern that has been created. This is sometimes done to, for example, help a company remain on an index like the FTSE. These indices give great exposure – almost like free marketing – but they have volume requirements. We saw this in a 2021 FCA enforcement where an individual was fined and prohibited from trading after they had utilized an abusive trading strategy to ensure that a minimum volume of shares were traded each day to stay on the FTSE All Share Index.

This form of market abuse is also known as scratch trading, wash sales, parking, circular trading, pooling and churning, and pre-arranged trading.

Although financial firms may have policies in place stating that employees are prohibited from conducting Wash Trading, it is crucial that they use trade surveillance and communications monitoring to detect potential Wash Trading from employees or clients.

Who is at risk of Wash Trading?

Any company where employees trade securities on behalf of the organization or its clients are at risk of Wash Trading. Companies can also become susceptible to Wash Trading through the general public or employees who trade in their listed securities from personal accounts.

What are the rules surrounding Wash Trading?

In the US, Wash Trading was first banned by the government with the passage of the Commodity Exchange Act in 1936. Today, Commodity Futures Trade Commission (CFTC) rules also prohibit brokers from profiting from Wash Trading, even if the firm says they were not aware of the trader's intentions.

It is routine for the US Securities and Exchange Commission (SEC) to prosecute Wash Trading under Section 17(a) of the Securities Act of 1933, and Section 10(b), and Rule 10b-5 of the Securities Exchange Act of 1934.

In the UK, Wash Trading falls under the Market Abuse Regulation 1.6, which focuses on market manipulation practices.

It is defined as: “a sale or purchase of a qualifying investment where there is no change in beneficial interest or market risk, or where the transfer of beneficial interest or market risk is only between parties acting in concert or collusion, other than for legitimate reasons”.

The EU defines Wash Trading in the level three material of the Market Abuse Directive and the detail of the Market Abuse Regulation.

This form of market abuse made the headlines during the early days of high-frequency trading – around 2012-2013 – when electronic trading programs were able to buy and sell securities at unprecedented speeds. The latest incarnation of Wash Trading is happening on many cryptocurrency exchanges, which is causing price transparency issues in those venues.

Is Wash Trading a prominent focus of regulators?

Regulators – particularly in the US and the UK – are now deploying sophisticated market data analytics (sometimes called SupTech) to identify all forms of market abuse, including Wash Trading. Never before have regulators had such technology firepower at their disposal to combat market manipulation.

The UK Financial Conduct Authority (FCA) receives more than 30 million transaction reports and over 100 million order reports a day which are analyzed and scrutinized to identify market abuse and manipulation. The FCA also receives around 90 suspicious transaction and order reports (STORs) per week, and these are also reviewed for potential misconduct and crime.

In the US, the SEC has also heavily invested in technology to improve the supervision of financial services firms and relies on trade data, regulatory reporting information, and other sources of data to perform these analytics. The SEC’s NEAT tool (National Exam Analytics Tool) reviews trade data from investment advisors and broker-dealers, while the ATLAS tool looks for insider trading before a major equity event to spot insider trading. Its High-Frequency Analytics Lab (HAL) is deployed to detect issues in high-frequency trading.

This means that many financial services firms are finding themselves in the awkward position of having regulators who are, in some instances, better at spotting market manipulation and abuse among the firms they regulate than the firms themselves. As such, the consequences of non-compliance are increasing as it is less easy for firms to hide – given the regulators’ data-driven approach.

Wash Trading Enforcement Examples

Wash Trading scandals can have a serious impact on financial services organizations. In March 2021, the CFTC ordered one cryptocurrency exchange to pay $6.5 million for false, misleading, or inaccurate reporting and Wash Trading – this resulted in that exchange postponing its own NASDAQ listing.

In June 2022, the CFTC sued another cryptocurrency exchange for making false and misleading statements in relation to a bitcoin futures contract, and for allowing its own clients to create a false market through Wash Trading. This made headlines around the world in part because of the exchange’s famous owners.

Wash Trading can also have a devastating impact on employees caught engaging in this practice. In one recent Wash Trading case in the UK, an employee was fined more than £50k and prohibited from performing any functions in relation to regulated activity. In another, the CFTC fined a firm $100,000 for Wash Trading and other market manipulation practices, while at the same time the group, who are owners of commodity exchanges, issued a Notice of Disciplinary Action with a fine of $25,000 and a 10-day suspension for one individual, and a fine of $10,000 with a 10-day suspension for another individual.

Firms are also being fined by regulators for not having robust market abuse detection and prevention programs in place. For example, a tier one bank was recently hit with a £12.6 million fine for Market Abuse Regulation compliance failings by the UK FCA.

How to detect Wash Trading and other Market Abuse Behaviors

To detect Wash Trading, firms should look out for unusual or atypical trading patterns among their traders – buying and selling in a brief time period that has no impact on the position or PNL of the entity.

A trade surveillance system with a Wash Trading algorithm can do this and help determine whether a specific pattern of activity is normal or atypical. Further, to help reduce false positives, a good trade surveillance solution should be able to filter for context – removing irrelevant results. In addition, the platform’s lexicon should be able to comb through voice and electronic communications for a wide range of search terms, including colloquialisms, to help tease out potential collusion with other traders.

Robust trade surveillance is one of the strongest tools that firms have for detecting Wash Trading – and given how much focus regulators are placing on this area of data analytics, it’s important that firms get this right.

Once a firm has discovered a case of Wash Trading, it should report it to the regulator as soon as possible, and take the necessary legal steps to undo any harm the activities have caused. The firm should also review its compliance program and processes to better understand if there were weaknesses that enabled the Wash Trading to take place.

What are the best practices for Wash Trading detection?

Here are some best practices for establishing and maintaining effective surveillance controls:

Financial firms need to be aware that Wash Trading may be taking place within their organizations. Many regulators – armed with SupTech – are now detecting market abuse ahead of the firms they regulate, and financial firms need to catch up.

To identify Wash Trading, firms need to be sure to implement best practices correctly – including trade and communications surveillance. These important weapons against Wash Trading should be tuned to detect Wash Trading and any other market abuse behaviors a firm is susceptible to given their trading model and activities.

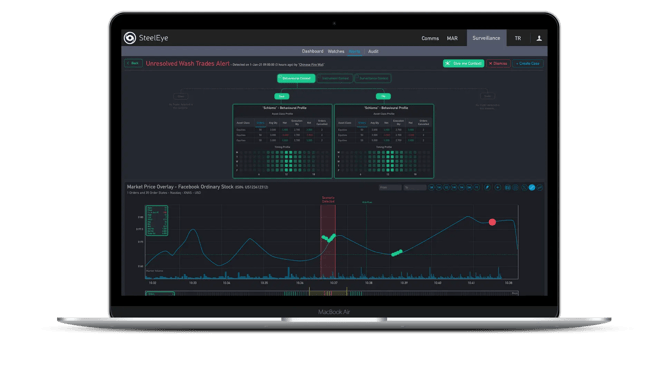

How does SteelEye enable firms to combat Wash Trading?

SteelEye provides robust and efficient solutions for identifying, investigating, and reporting instances of market abuse.

Our trade surveillance suite has algorithms specifically designed to spot Wash Trading across all transactions and covers a range of other abusive trading practices like layering, spoofing, insider trading, and more. SteelEye’s communications surveillance solution helps firms identify collusion and other forms of misconduct. In fact, SteelEye is the only platform that can natively bring together both communication and trade surveillance on one platform.

With SteelEye's fully audited case manager firms can effectively track and monitor their work queues, carry out market abuse investigations, and swiftly respond to regulatory requests. When an alert has been triggered, SteelEye’s case manager enables compliance teams to easily bring together all the information required for an investigation – including trades, comms, market data, and news.

Book a demo today